-

US ATTACK ON IRAN ROILS EQUITIES AND DEFENSIVE ASSETS

Data Sourced from FE Analytics, and Bloomberg Finance LP

US ATTACK ON IRAN ROILS EQUITIES AND DEFENSIVE ASSETS

This week’s US-Israeli attack on Iran caught markets off guard. Despite the significant military build-up, recent negotiations about Iran’s nuclear programme had appeared to be making progress and Donald Trump had made little attempt to talk up the case for an attack in advance. The administration’s justification remains muddled, with contradictory rationales still emerging. Markets have reflected that confusion as risk and defensive assets have sold off, an unusual combination suggesting broad uncertainty rather than orderly repositioning. Global equities are down, though modest losses in the US imply some investors expect a short conflict. Even traditional havens – Treasuries and gold – have declined.

Higher energy prices were inevitable given the region’s importance to global petroleum supply. A prolonged conflict risks shortages and would add inflationary pressure as energy and shipping costs push up consumer prices. However, despite the spike energy markets, prices are still far below the levels seen when Russia invaded Ukraine. And while equity markets have fallen this week, most are still positive year to date.

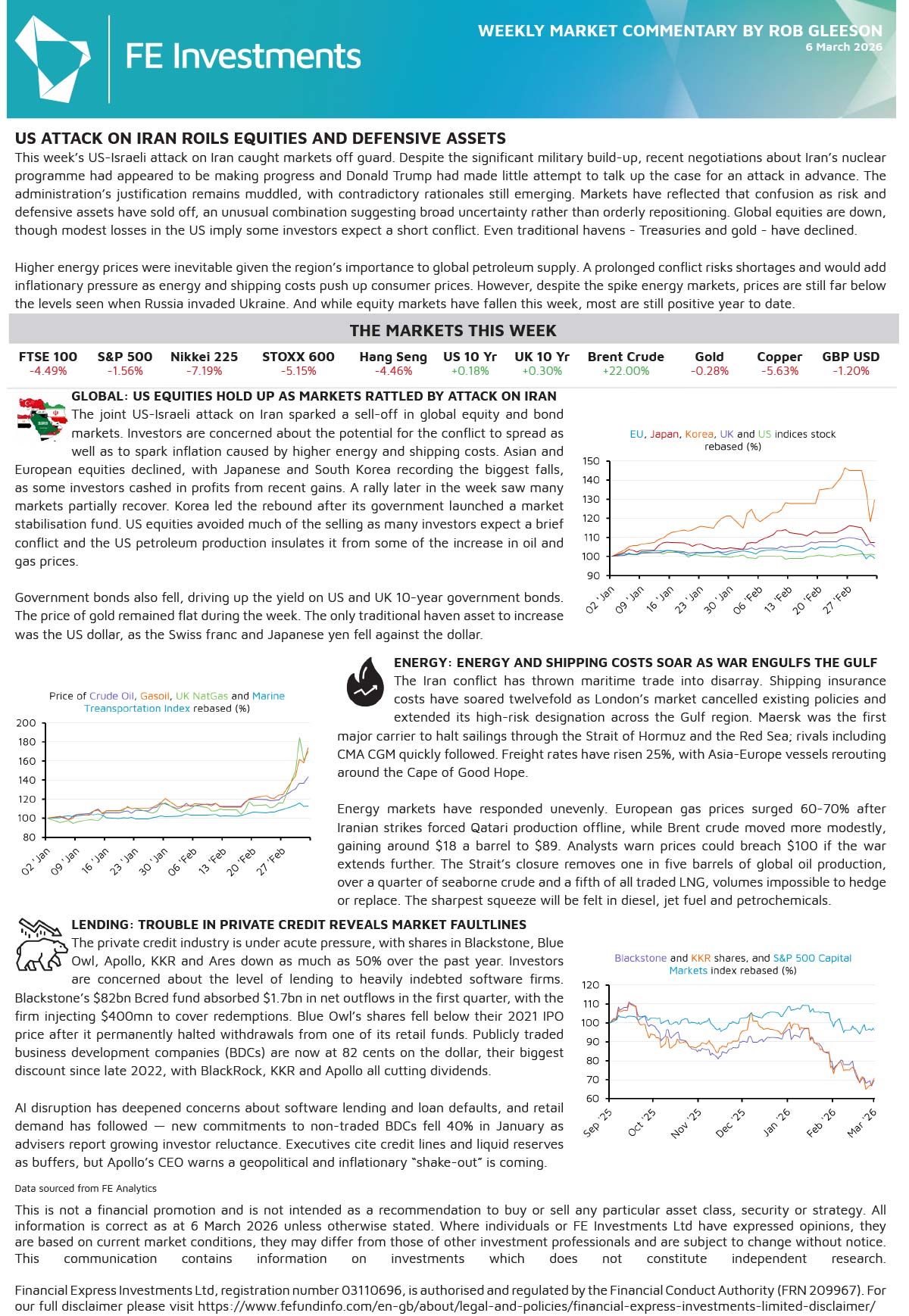

GLOBAL: US EQUITIES HOLD UP AS MARKETS RATTLED BY ATTACK ON IRAN

The joint US-Israeli attack on Iran sparked a sell-off in global equity and bond markets. Investors are concerned about the potential for the conflict to spread as well as to spark inflation caused by higher energy and shipping costs. Asian and European equities declined, with Japanese and South Korea recording the biggest falls, as some investors cashed in profits from recent gains. A rally later in the week saw many markets partially recover. Korea led the rebound after its government launched a market stabilisation fund. US equities avoided much of the selling as many investors expect a brief conflict and the US petroleum production insulates it from some of the increase in oil and gas prices.

Government bonds also fell, driving up the yield on US and UK 10-year government bonds. The price of gold remained flat during the week. The only traditional haven asset to increase was the US dollar, as the Swiss franc and Japanese yen fell against the dollar.

ENERGY: ENERGY AND SHIPPING COSTS SOAR AS WAR ENGULFS THE GULF

The Iran conflict has thrown maritime trade into disarray. Shipping insurance costs have soared twelvefold as London’s market cancelled existing policies and extended its high-risk designation across the Gulf region. Maersk was the first major carrier to halt sailings through the Strait of Hormuz and the Red Sea; rivals including CMA CGM quickly followed. Freight rates have risen 25%, with Asia-Europe vessels rerouting around the Cape of Good Hope.

Energy markets have responded unevenly. European gas prices surged 60-70% after Iranian strikes forced Qatari production offline, while Brent crude moved more modestly, gaining around $18 a barrel to $89. Analysts warn prices could breach $100 if the war extends further. The Strait’s closure removes one in five barrels of global oil production, over a quarter of seaborne crude and a fifth of all traded LNG, volumes impossible to hedge or replace. The sharpest squeeze will be felt in diesel, jet fuel and petrochemicals.

LENDING: TROUBLE IN PRIVATE CREDIT REVEALS MARKET FAULTLINES

The private credit industry is under acute pressure, with shares in Blackstone, Blue Owl, Apollo, KKR and Ares down as much as 50% over the past year. Investors are concerned about the level of lending to heavily indebted software firms. Blackstone’s $82bn Bcred fund absorbed $1.7bn in net outflows in the first quarter, with the firm injecting $400mn to cover redemptions. Blue Owl’s shares fell below their 2021 IPO price after it permanently halted withdrawals from one of its retail funds. Publicly traded business development companies (BDCs) are now at 82 cents on the dollar, their biggest discount since late 2022, with BlackRock, KKR and Apollo all cutting dividends.

AI disruption has deepened concerns about software lending and loan defaults, and retail demand has followed — new commitments to non-traded BDCs fell 40% in January as advisers report growing investor reluctance. Executives cite credit lines and liquid reserves as buffers, but Apollo’s CEO warns a geopolitical and inflationary “shake-out” is coming.

For more information regarding our weekly market reports, we encourage you to give us a call on 01732 746188 or send us an email at enquiries@foxgroveassociates.co.uk.

This document has been prepared for general information only. It does not contain all of the information which an investor may require in order to make an investment decision. If you are unsure whether this is a suitable investment you should speak to your financial adviser. This information is not guaranteed to be correct, complete, or accurate. Financial Express Investments Ltd, registration number 03110696, is authorised and regulated by the Financial Conduct Authority (FRN 209967). For our full disclaimer please visit https://www.fefundinfo.com/en-gb/about/legal-and-policies/.